This is a long-read. The short version is as follows.

- Two sectors of Ghana’s economy are specifically identified in the country’s recent IMF program for critical attention because of their contribution to the country’s debt debacle: energy and cocoa. The story of Tema Oil Refinery exemplifies what has gone wrong with Ghana’s energy sector.

- Tema Oil Refinery has big problems that require hundreds of millions of dollars and sophisticated investors to fix.

- Such money and investors will not come unless the country’s leaders are genuinely interested in an above-board transaction, and are willing to spend the taxes they have collected in TOR’s name to clear the muck and give serious investors a fresh chance. It is clear that they are not. They are only interested in a deal that will keep their cronies positioned at vantage points.

- So, for many years, various shady deals and shadowy investors have been paraded as saviours of TOR, of which the latest are Decimal, Legacy and Torentco.

- None of these entities have what it takes to truly revamp TOR. The opacity, underhand dealings, shadiness and murkiness risk becoming a breeding ground for criminal and underworld activities, destroying what little reputational value remains in TOR. Already, there are fears that some of the partners proposed for the Torentco transaction may be embroiled in sanctions-busting activities.

- An open and competitive process should be pursued to bring fresh management not beholden to any political elite factions. The unencumbered management should be empowered to run a totally above-board process to attract investors with deep pockets. Accompanying energy sector reforms, strict use of energy taxes for their intended purpose, and strict price deregulation would need to be in place to assure such investors.

- Any shady leasing of assets to shadowy operators will lead to the compounding of TOR’s debts, continued obsolescence of TOR’s infrastructure, and an eventual reckoning in which the company’s situation becomes irredeemable and unsalvageable.

The Tema Oil Refinery (TOR), located in the country’s coastal industrial base, is a product of Ghana’s post-colonial industrialisation drive that saw the first government after independence engage international investors as strategic partners in a number of vital industrial projects.

The same process that brought foreign financiers and engineers to build, own and run TOR in 1963 also gave Ghana the Volta Aluminum Company (VALCO), Akosombo hydroelectric dam, and Ghacem, still among the most important anchors of Ghana’s industrialisation dream.

A wave of nationalisation, however, swept the country in the 1970s and by April 1977 TOR was fully state-owned. It is a sad testimony to the perennial decline of state capacity in Ghana that since then TOR has lurched from one crisis to another.

The Rude Awakening

From the point of nationalisation onwards, the refinery did not see any serious renovation or capacity boost until 1989. Even then it was widely recognised that capacity expansion and technological retrofitting and upgrading were essential to the ongoing viability of TOR. But then again a long list of state-run industries were in the same boat.

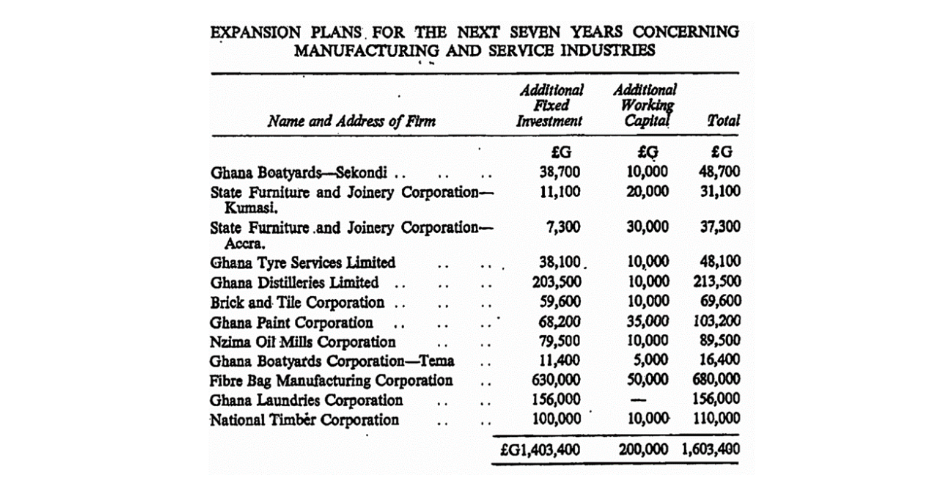

In 1963, when the seven year development plan was launched, several state-run industrial concerns were placed on a list for capacity expansion and upgrading by 1970 at the cost of £1.6 million ($4.5 million), or the equivalent of $45 million in today’s money. By 1992, not a single one of them had seen any serious investment for transformation.

Halting steps to redemption

A $200 million loan from Korean investors enabled the expansion of the Tema Oil Refinery (TOR) to its current 45,000 barrels per day capacity by the late 1990s.

When a new government took over from the Rawlings government in 2000, a long courtship with Korean government and private entities, especially Samsung, ensued. At stake was a fresh $230 million loan for the long anticipated expansion and addition of modern modules to handle a wider range of crude oil types. TOR’s precious Residual Fluid Catalytic Cracking Unit (RFCC) was eventually financed by Samsung from the loan package and commissioned in November 2002. By this point, the refinery had racked up debts of over $300 million.

In 2003, the government instituted new taxes to enable the refinery pay off its debts and complete the planned expansion works.

Energy Analyst, Dramani Bukari, estimates that after these expensive technical works, plant utilisation (how much of a factory’s theoretical capacity can be practically used) at TOR ramped up to a high of 80% before beginning a disorganised descent until it hit a rock-bottom of 19% in 2009.

![]()

Clearly, despite absorbing tens of millions of dollars in investment for technical transformation, TOR was still struggling with viability issues, increasing the urgency for a more radical expansion program to improve unit economies. Officials mooted the prospect of adding 100,000 barrels per day of refining capacity at the cost of ~$200 million.

Meanwhile, the debts continued to mount. Politicians continued to interfere in the running of the organisation, only ever appointing cronies and allies to all Board and senior management positions. Management policies grew even more arbitrary. Underfunded government subsidies ensured that the same year TOR processed the most crude, 2004, it also recorded the highest losses for the decade. Samsung, tired of all this drama, withdrew its interest as a prospective strategic partner.

The bumbling continued. Despite collecting $500 million in TOR-focused taxes by 2008, the government refused to invest any significant amount of money into the facility, even as it toured the globe looking for so-called “partners”. Unwilling to fully let go of a juicy gravy train, open and competitive privatisation was never really placed on the cards.

So, by 2010, the debt had ballooned to $1.4 billion. Confronted with the prospect of total shutdown and hostile creditor actions, the government started to make some payments. GCB, a state-controlled bank and a captive TOR creditor, was on the verge of being pulled down with TOR forcing the government to arrange a $316 million repayment.

That however did not stop the refinery from shutting down.

Facing a loss of public credibility, the government doubled down on efforts to address the fundamental issues.

By 2015, further payments had brought the debt down to a little under $750 million. Yet, frequent announcements of “strategic partnerships” and financing deals had yet to bear fruit. In one particularly striking example, the government announced a $900 million financing package in 2012 to tackle the crushing working capital constraints of the company.

Nothing of note happened.

God bless our hustle

Months later, in 2013, TOR was back to hustling for crude parcels around the world to keep the refinery in business.

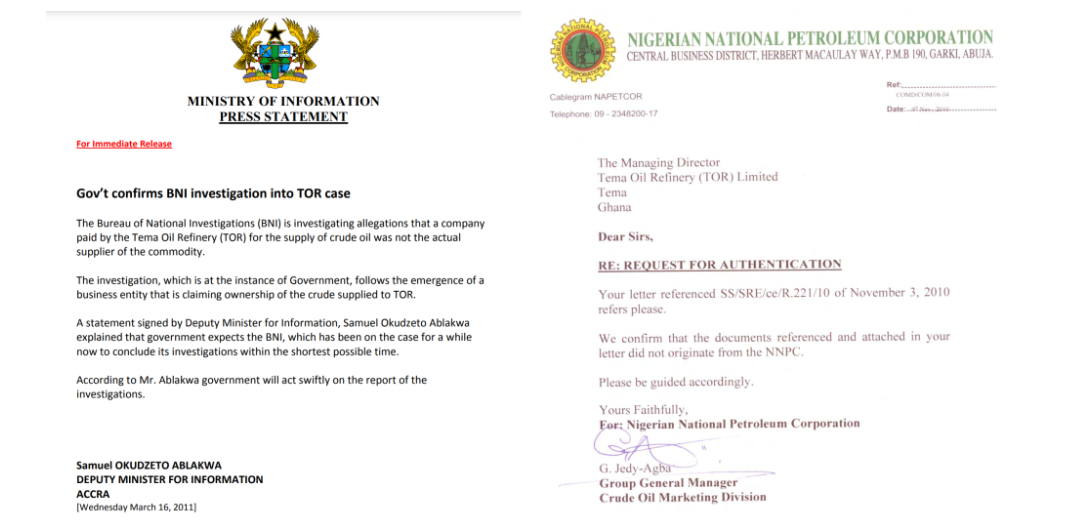

The culture of hustling for crude and bits and pieces of working capital was fast becoming the defining hallmark of the TOR story. In 2011, a bizarre drama unfolded in which fake companies popped up from the undergrowth to claim ownership of crude oil delivered to TOR, forcing the intelligence services to step in.

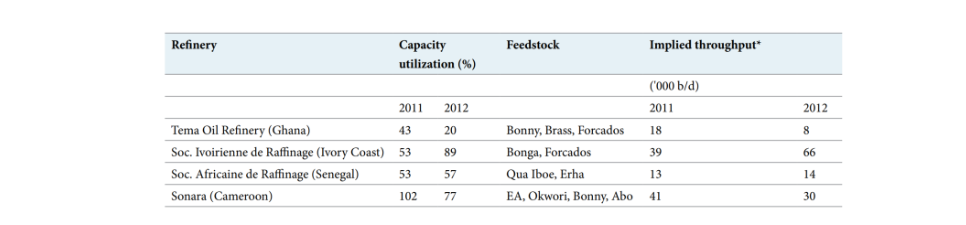

Meanwhile, TOR’s throughput was now the lowest among peer refineries in the subregion.

In 2015, another effort was made to raise domestic funding to tackle the TOR debt and capacity juggernaut, but this time in concert with other energy sector challenges. The Energy Sector Levies Act (ESLA) was passed and, in 2017, a special purpose vehicle created to transform taxes into a more effective financing mechanism for clearing legacy debts and freeing energy sector corporations like TOR to embark on structural reform. Recall that by this time, TOR’s debt was around $750 million.

The ESLA SPV raised a total of $1.6 billion in the three years following setup. The government simply expanded its general spending and devoted nothing to the structural transformation of the refinery. It did however clear a significant portion of TOR’s legacy debt, which thus dropped to $460 million.

TOR revenues, on the other hand, tumbled from a peak of ~100 million in the last decade to less than $25 million in 2020. Accumulated losses over the period exceed a billion dollars.

Today, our sources tell us that TOR’s books have not been properly audited but provisional figures show a debt of nearly $450 million. The spate of shutdowns have intensified over the years leading to a state of near mothballing, with refining activities at a standstill for an unprecedented 26 months now. The organisation is on its fifth or so Chief Executive in five years. The center cannot seem to hold.

The Shadowy Duo: Decimal & Torentco

It is against this background that civil society activists and analysts received with dismay news of the submission to the Public Procurement Authority (PPA) of a proposal by the TOR management to lease the main assets of the refinery to a shadowy entity called Torentco Asset Management (“Torentco”) for six years. To fully appreciate the concerns of the analysts over this matter, it is important to recap the key issues.

- It has long been recognised that TOR’s working capital, refurbishment, and debt management require capital in the range of between $500 million and $1 billion to begin to get a handle on the structural viability of the refinery. And that considerable capacity expansion is essential. In fact, the last CEO at TOR to have had anything remotely approaching a normal tenure insisted that $3.5 billion was required to start from a clean slate.

- It is also widely accepted that TOR’s simple initial design as a hydroskimming plant requires a substantial overhaul to lower conversion losses and sustain plant utilisation over the medium term. For example, TOR’s current configuration is optimised for heavy distillates hence the criticality of the RFCC. Gasoil and atmospheric residue constitute more than 60% of its output. To produce more of the products most required on the domestic market such as petrol (Premium Motor Spirit) and diesel, a robust RFCC is vital in TOR’s current configuration.

- TOR’s adverse managerial and operational history makes it difficult to raise money on good terms, obtain feedstock (raw crude) on reasonable credit, and to respond to market dynamics in a commercially competitive manner.

For nearly two years now, the government and TOR have been promising a major deal with the features needed to tackle these serious challenges. Things seemed to have come to a head when in another of the frequent managerial reshuffles TOR has become famous for, a new CEO took the helm last year and promptly announced a strategic partnership with a little known Kenyan entity called Decimal Capital to turn the refinery around.

Decimal was clearly introduced into the mix by another short-lived CEO of TOR, who was removed following a civil charge by the United States government for various alleged offences. He was subsequently criminally indicted under the Foreign Corrupt Practices Act. Many analysts believe that Decimal was still being teleguided by this former CEO.

This week marks one year since TOR’s management announced to the country that the Minister of Energy has approved a strategic partnership agreement between TOR and Decimal for the former to lease its infrastructure for the use of the latter in order to resume stalled refining operations. Then everything went quiet. At the time, Vitol was mentioned as the commodity financier. That is to say, Vitol, a large Swiss energy trader, was to provide the raw crude for TOR to refine on flexible financial terms. Nothing was heard of that either.

It is now apparent that there are factions in the highest echelons of the Ghanaian government, each with its own preferred crony arrangement. Because at the same time the nation was being told that TOR was moving forward with Decimal, another shadowy group calling itself Torentco was also engaged in brisk negotiations with TOR to lease the very same assets supposedly being transferred to Decimal. As is typical with these crony arrangements, no information was made public about any of these developments even though TOR is a 100% state-owned enterprise under an active tax-supported bailout.

Torentco Ascending

After months of factional infighting, during which more shadowy groups, like a certain “Legacy Capital” based in Dubai and led by a certain Vladimir Palikhata (an occasional name in Russian whitecollar crime sagas) burst onto the scene, the Torentco group suddenly gained an upper hand.

On 13th June, 2023, TOR, presumably tired of dragging its feet, sent an updated proposal to lease certain of its vital assets to the Public Procurement Authority for ratification on a single-sourcing basis, the preferred procurement model when shady things are underfoot.

Torentco’s offer to TOR can be summed up as follows.

▪︎ TOR’s main productive assets will be leased to Torentco for 6 years. Excluded from the transaction are TOR’s creaky laboratory; TOR’s stake in the company (GPMS) that manages the moorings for marine vessels discharging cargo into TOR and the facilities of other bulk oil operators; TOR’s permits to use certain infrastructure it does not own but need for its work (“rights of way” and “tie-ins”); and the RFCC, a secondary plant at TOR that can extract valuable products from leftovers of products made in the primary plant, the CDU. Whilst these auxiliary facilities will not be leased out, and thus TOR will preserve the associated revenues of about $12 million, Torentco will nonetheless have access to them as and when necessary.

▪︎ Torentco is allowed to refine up to 8 million barrels of oil a year by paying $1 million every year as annual rent.

▪︎ There is also an “additional rent” amount of $1.067 million per month. The strategy behind this rent split is obscure, but Torentco argues that it is necessary to protect TOR’s lease revenue from creditors, who apparently have been trying to to attack TOR’s assets for monies owed.

▪︎ If Torentco refines more than 8 million barrels, it pays $0.5 for each extra barrel.

▪︎ So, if Torentco stretches the refinery to its full limit and refines 16.5 million barrels, it pays $17.2 million in rent.

▪︎ Torentco will invest $22 million to revamp the refinery. On top of that, it will assume responsibility for clearing provident fund arrears up to the tune of $2.5 million. To date, TOR has been struggling to pay its SSNIT and pension liabilities.

▪︎ Torentco will furthermore pay $800,000 into a reserve fund plus $0.4 to cover maintenance expenses for every barrel refined, while assuming responsibility for insurance and utility payments. At maximum production limit, Torentco’s maintenance commitments will cost about $7.4 million and insurance expenses will hit about $6 million per annum.

Beyond the core offer, Torentco has sought to bolster its proposal by name dropping certain partners. Vitol has been mentioned again as a potential bulk buyer of the refined output. Two local engineering and construction companies have been introduced as technical contractors for the refurbishment activities: ENTTP and Litwin Engineering. Rounding up the list of proposed consortium members is a commodity supplier called Pontus.

The PPA Board convened a meeting on 15th June, 2023, to deliberate on the updated proposal. Rather than comment substantially on the Torentco offer based on its Board’s due diligence findings, the PPA simply took a leaf from the book of the biblical Pontius Pilate when he sent the condemned Christ to Herod Antipas, King of Galilee. The PPA says that it took note of what it saw as “partnership” elements in the proposed transaction and thus chose to refer the matter to the Ministry of Finance, which under Act 1039 is responsible for scrutinising Public Private Partnerships.

But there was much more to say about the transaction beyond administrative formalities.

What is wrong with the Torentco Deal?

The Torentco deal is anchored on the fact that TOR today is idle for all the reasons and factors this essay has traversed. Given that TOR has been mismanaged into a state of near comatose and its own sole shareholder – the government of Ghana – has publicly announced that most of its frontline management are thieves, Torentco reckons that no serious investor will come in.

In these circumstances, Torentco’s mastermind, Michael Darko, ably assisted by his trusted sidekick, George Antwi, are completely convinced that TOR has nothing to lose if it carves out its productive assets and turn them over to a non-tainted operator to make a bit of money. Money that will be shared with TOR even as the latter continues to waffle around awaiting its salvation.

Despite the cosmetic plausibility, there is serious short-sightedness in such a proposal.

- First, neither Mr. Darko nor Torentco ring any bells in the energy investment corridors at home and abroad. If the whole strategy hinges merely on hiving off TOR’s assets into a separate legal entity, then TOR might as well create such a subsidiary itself.

- The issues of where working capital, a sustainable commodity supply contract, and credible offtaking arrangements will come from can only be properly addressed by a credible entity. TOR may not be one, but neither is Torentco.

- None of the companies Torentco has mentioned, except Vitol, ring any bells either. And our sources in Vitol say no conclusive offer is on the table. ENTTP and Litwin are not the heavyweights needed to turn around a contraption as stuck in the swamps as TOR.

- ENTTP’s Christopher Hesse-Tetteh has been mentioned in connection with some general logistics and construction works, but nothing remotely approaching the complexity and technical risk presented by TOR.

- Litwin Engineering claims to be based in Switzerland but has zero footprint in the energy consulting and financing space except its own scanty self-attestations online.

- The most worrying aspect of the Torentco Consortium’s credentials for this activity is its proposed source of crude oil feedstock. After all, it is inability to raise letters of credit to import crude to refine and pay off creditors that began TOR’s spiral of death. Only two entities fit the Pontus profile mentioned in Torentco’s proposals. Both are embroiled in shady oil trading situations, touching on potential fraud, sanctions busting and even terrorism. They are Pontus Trading of Dubai and Pontus Navigation of the Marshall islands.

The last issue goes to the heart of the credibility, transparency, and above-board concerns that civil society activists and analysts have about the whole leasing transaction. Actors lacking mainstream commercial credibility more easily fall prey to the wiles of the criminal and/or unethical underworld.

The bare economics are wobbly

Some have tried to position the proposed Torentco leasing strategy as nothing more than a variant of the tolling transactions TOR has had with the likes of Total, Woodfields and Vitol over the years. Such analysis is wrongheaded.

A leasing contract involves a handover of substantial control. A tolling contract does not. Once Torentco or another party gets hold of the refinery, it retains every right to secure its own commodity supplies, refine, sell, and pay back the supplier the cost of the crude oil, pocketing the full margin. There is nothing that says that such a company must limit itself to tolling deals with well known commodity suppliers like Total and sell to well known traders like Vitol. It can seek to maximise its margins by obtaining crude in grey markets to refine and sell back into such grey markets, especially in countries with porous supply chain security that cannot police even unsophisticated gold smugglers.

The sheer amount of money (crude calculations suggest between $250 million and $750 million in the TOR case depending on precise mix of refined products and plant utililisation) that can be made in today’s geopolitically fraught oil market if one can get shady oil to refine, sell and pay back over an extended credit period would be enough to corrupt multiple safeguarding institutions and overwhelm the country’s risk management capacity.

Per Current Proposal, there’s no scenario in which TOR comes up tops

But even if we were to take Torentco’s word for it that they intend to play within the traditional tight-margin refining space by simply cutting through TOR’s bureaucratic inertia and ringfencing the toxic legacy constraints such as debts and bad commercial reputation, the offer as it currently stand does not add up.

The actual guaranteed payments (direct and indirect) to TOR are equivalent to less than $1.5 per barrel, and thus lower than the tolling fee offers previous CEOs refused to accept. It is far lower than the $4.5 that those CEOs believe is the minimum sensible rate given the context.

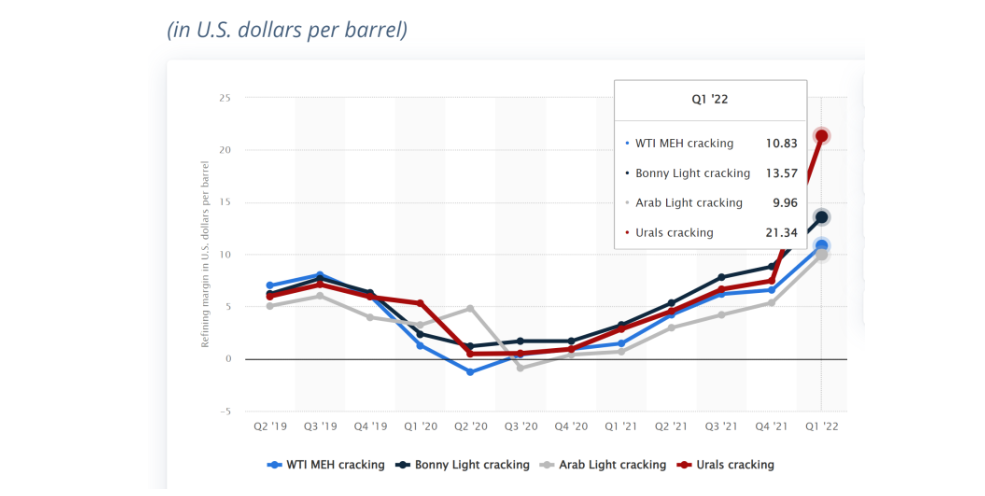

In a situation where tightness in global oil supply, ahead of the electric car transition in future years, starts to provide support for $15 per barrel average refining margins in the next five years, a refinery operator would be in a good place to secure its commodity supply by whatever means. In such a world, the incentives are heavily skewed in Torentco’s favour.

Source: Statista

The risks, on the other hand, weigh heavily against TOR. Its debts will be compounding, since it will not receive anything close to what it needs to service them whilst its productive assets remain encumbered for 6 years. Let us be clear. The kinds of money Torentco is mentioning – $22 million upfront investment, ~13 million in annual rent etc. – do not even begin to make a dent in TOR’s real financing needs. As recounted in the early sections of this essay, TOR requires a solution that yields many times more.

And, should the unthinkable happen, and the refinery find itself enmeshed in some sanctions-evading scandal because of shady suppliers or consortium members, and gets blacklisted, the burden of salvaging the tattered remains of its reputation will also fall on TOR, not Torentco.

There is no point in mincing words here. The Torentco deal as it stands now is not in TOR’s interest. It is absolutely not in Ghana’s interest. A whole load of transparency, open scrutiny, and reworking is required before it can even be taken into serious consideration.

Source: Bright Simons

Source: citifmonline

Comments