If you are a certain age and live in Accra, Tema, Kasoa, Takoradi, and their environs, there was probably a time when you thought Surfline was like, man, going to bankrupt MTN & Vodafone for real.

Nowadays, I hear folks on social media cursing and cussing, and shaking their fists at their Surfline modems gathering dust on corner stools. Some bought into the euphoria at its peak. And now the bloody devices won’t connect,

How we got here is both thrilling and tragic.

1. The spunky startup was founded in 2011 by one of Ghana’s most formidable fuel and real estate magnates. The company’s impetus was a new policy by the government to limit 4G broadband internet provision to local, Ghanaian-owned, companies. The big telco incumbents, all foreign-owned, were to be denied.

2. In 2013, Surfline and Blu were given shiny new 4G licenses, at $6m a pop. The next year, Surfline launched in Accra with support from Alcatel, IBM, Oracle, etc. It was a big deal. The only 4G network in West & Central Africa, that was the story.

3. In the ensuing years, other licensed local 4G players went live: Blu, Telesol, Broadband Home, and Busy Internet. Goldkey, one of the early licensees, however, did not. Its owners chose to wait and see.

4. By June 2016, Surfline had ~81k subscribers, representing ~75% of the entire broadband 4G internet consumer base in Ghana. It was on course to $100 million in annual revenue, a major milestone on its medium-term commercial roadmap.

5. But what politicians give, they can also take away. That same year, the policy changed. The government decided to allow the big telcos to play in the 4G space.

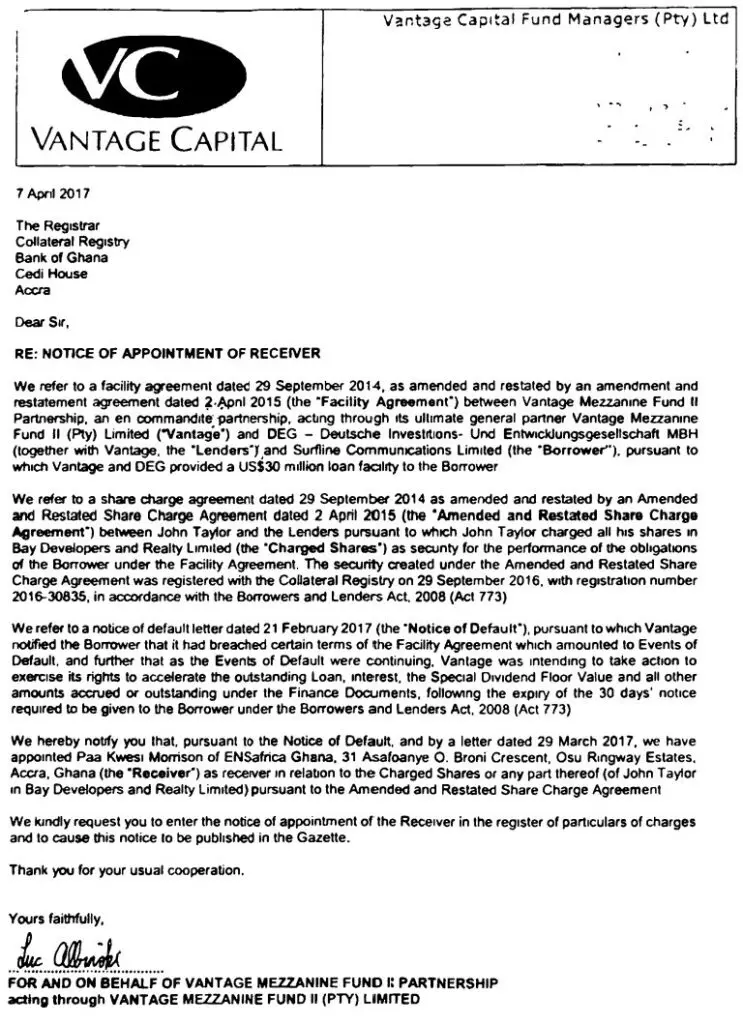

6. Surfline, all this while, had been burning cash fast. To sustain growth, it approached a South African investor, Vantage. Vantage brought the German Development Fund (DEG) (part of the behemoth KFW group), on board.

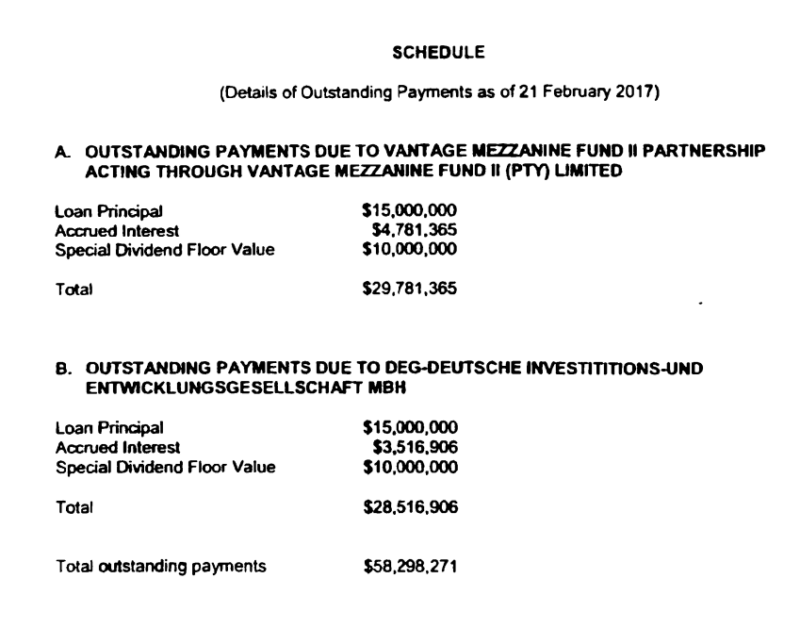

7. Thus, in 2015, Surfline raised $30m from two foreign investors, guaranteed with the personal assets of its founder. The facility had a 5-year term and a dollar interest rate of 12%, to be jacked up to 15% if any interest payment was missed. A guaranteed minimum dividend of $10m linked to convertible equity was also in the mix.

8. MTN’s entry in February 2017, however, blocked further growth for all 4G broadband internet operators. Surfline began its terminal decline. By December 2020, it had lost 50% of its subscribers.

9. The shrewd real estate magnate and fuel nabob behind Goldkey took one look at the whole affair and simply sat on the license. At the first opportunity, he flipped it to MTN and recouped his money.

10. Blu, which never really signed on more than 1500 customers throughout its rocky journey, left the scene around April 2021.

11. By December 2022, Broadband Home was down to less than 300 subscribers countrywide. Busy had given up the ghost a few months earlier. Telecol limped on till January 2023 and then bit the dust. MTN reportedly lapped up most of the licenses of these dead pioneers, thus increasing its spectrum resources, whilst its executives sang Master KG’s Jerusalema.

12. Four months later, in May 2023, Surfline’s creditors finally pulled the plug. Its data centres and masts are powered down. Modems, dongles and MiFi pads blinked, sputtered, and also went offline in over 30,000 homes. The telecom regulator, NCA, mumbled something about “investigations” when folks pressed about their prepaid, now apparently worthless, credit on their Surfline devices.

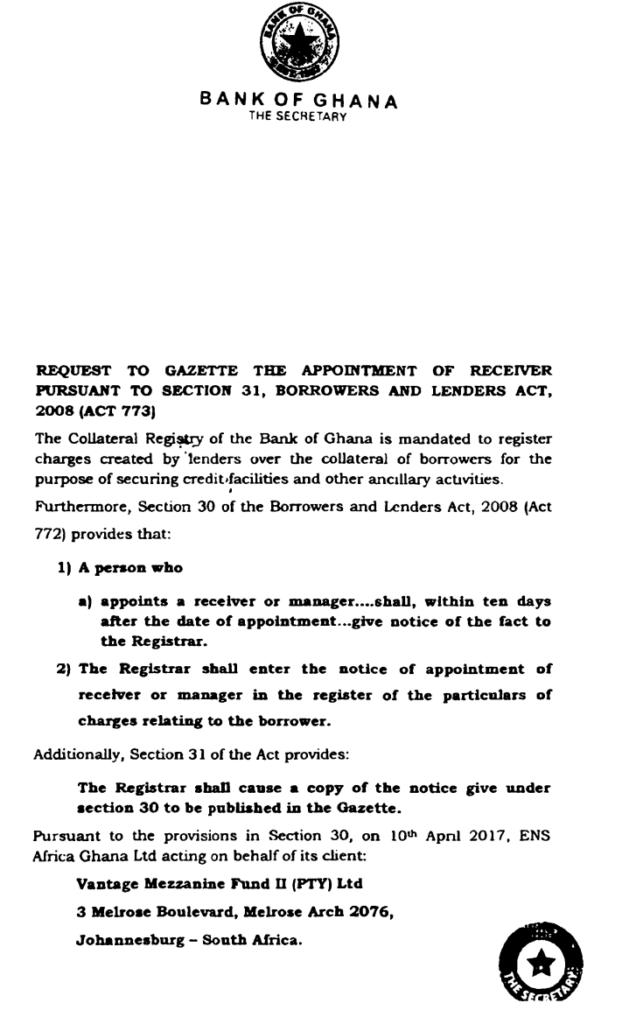

13. For most Surfline subscribers, this is the story as they know it. But there was another tragic timeline. As the company started to bleed, it missed interest payments to Vantage in 2017 setting off a chain of events, which will lead to the founder’s real estate empire, Bay Developers, being taken over by the investors.

14. The takeover of Bay Developers, at a valuation of $15 million, was supposed to be part of a broader settlement of the indebtedness, in which shares of Surfline were to be transferred to Vantage and DEG, and the personal guarantee of Surfline’s founder vacated. A settlement agreement and consent judgment would even be secured to this effect.

15. However, as the company’s operational challenges deepened and debt piled up, an incoming strategic investor, the Botswana Development Corporation, backed off. Seeing as the transfer of shares from Surfline to Vantage had been delayed because, according to Surfline’s principals, a no-objection was being sought from another investor, Vantage wrote to Surfline in June 2018 to revoke any commitment it had to a settlement that will extinguish the guarantee. All this drama while interest was compounding like mad.

16. Vantage was now committed to doing everything to collect the outstanding amounts. Having sent a letter to Surfline in July 2018 calling on the guarantee, it shifted to a war footing.

17. The next year, in 2019, DEG also declared a default on its $15 million portion of the facility. The total amount due DEG at this point was ~$34 million. Such is the power of compound interest.

18. Surfline was under massive competitive pressure from the big telcos all through this ordeal. Faced with savage odds on all fronts, it chose to double down on promotions to win market share and grow revenue.

19. In early 2021, Vantage was all set for war. It demanded that the accumulated interest and dividend of $27 million be paid in full. Then it activated the arbitration clause in the facility agreement. It also engaged DEG, and after discussions had the DEG portion of the facility assigned to it. 20. Surfline decided to fight back by suing Vantage in the Ghanaian courts and demanding that an injunction be placed on the arbitration process in London. That matter, in the usual fashion, soon got bogged down in the courts as the arbitration proceeded unabated.

21. In December 2022, after nearly two years of arbitration, the single arbitrator concluded that Surfline’s founder was personally liable for ~$59.4 of liabilities. The amount is to accrue interest of 15% annually from October 2022 so long as it remains unpaid.

22. The Founder of Surfline naturally feels aggrieved. He borrowed $30 million. He has been forced to hand over his real estate company to pay half of it. He was willing to relinquish equity in the business to the lenders to satisfy the remainder of the obligation, and perhaps even trade more for additional cash infusion. Instead, he is now saddled with over $70 million in debt and the corpse of a company. Unsurprisingly, he refuses to pay.

23. Vantage (also acting on behalf of DEG) are, on their part, determined to collect every cent. In their view, Surfline’s execution had been shoddy, and poor strategic choices, including failing to agree terms with the Botswanans and the decision to force out a strong CEO, had led to the squandering of their investors’ money.

24. So, we have an irresistible force in an encounter with an immovable object. Vantage has been scouring the Earth looking to trace and locate assets belonging to the Founder of Surfline and seize them. From Barclays bank accounts in the UK to various assets in Italy, Bermuda, Malta, and elsewhere. Its latest assault happened just two and half weeks ago, in the United States. It has eyes on a certain plump Bank of America account in New York belonging to their antagonist.

25. Throughout the arbitration proceedings it became clear that the wording of the loan agreement had received very limited input from the borrower. As is typical, the lender had crafted powerful covenants that bind like demonic chains. To the extent that arbitration tribunals and courts these days focus a lot on the “construction” of terms and provisions in contracts, Surfline’s founder had almost no chance of extricating himself.

26. If you are an angry Surfline customer, I suppose you now have some additional context as to how your credit is useless.

27. Business is war everywhere. In Africa, it can be Armageddon. And, as they say, you can always tell the pioneers by the arrows in their back.

Comments